12 E 49th St., 11th Floor, New York, NY 10017

T: +1-212.323.7000

E: info@roundtables.us

November 29, 2023

California’s Homeowners’ Insurance Crisis: The Catalyst to Really Transform Claims

The increased frequency and severity of wildfires and other natural weather disasters has brought the California home insurance marketplace to its knees.

Earlier this year, several large insurers—State Farm, Allstate, Farmers Insurance Group, American Family, Nationwide, Erie Insurance Group, Berkshire Hathaway, AIG and Chubb—announced they would stop issuing new homeowner’s policies and would not renew existing ones in California. Because of lag times between insurance rate requests and rate approvals, insurers stated they no longer wanted to rely on traditional products and rate lines in areas where wildfires and other natural disasters occur.

In late September, California’s Insurance Commissioner proposed letting insurers consider climate change when setting their prices. Unlike other states, California does not let insurers consider current or future risks when deciding how much to charge for an insurance policy—historically, the only factors considered have focused on what has happened to the property itself, such as the addition of a new pool, to set the price of the insurance policy.

Pricing Risks & Modelling

“There are no bad risks, only bad pricing,” says Karen Clark, co-founder and chief executive of risk modelling firm Karen Clark & Company (KCC), in the Intelligent Insurer. Clark also noted that risks once categorized as ‘secondary perils,’ such as wildfires, wind, and water need to be “reassessed and reprioritized.”

The probability of $10-20-30 billion losses is increasing in this so-called ‘secondary peril’ category: “We’re always talking about the protection gap in the industry as a whole and we like to think of that as being in developing economies,” Clark added. “But even in the US the protection gap is growing. It used to be focused on flood and earthquake and now you’re seeing it on wildfire and hurricane coverage.”

Patrick Kelahan, co-founder of The Insurance Elephant Company, commented in Digital First Magazine that the current challenges in the Florida and California home insurance markets require macro changes in how property insurance is designed and distributed. “Not doing something is impractical, but continuing traditional programs is financially foolhardy,” Kelahan said.

Kelahan concluded that this might be the time to revisit the design of property insurance and leverage more sophisticated analytical methods to look at property risks in a property-by-property risk analysis.

The Critical Role of Claims

At the heart of the insurance business is claims. Yet most of the focus on insurance transformation has been on the customer experience. According to the 2022 U.S. Claims Digital Experience Study by J.D. Power, insurers meet customer expectations just 34% of the time. What is causing the disconnect between the technological efficiencies of settling claims and the insured’s perspective of the claims experience?

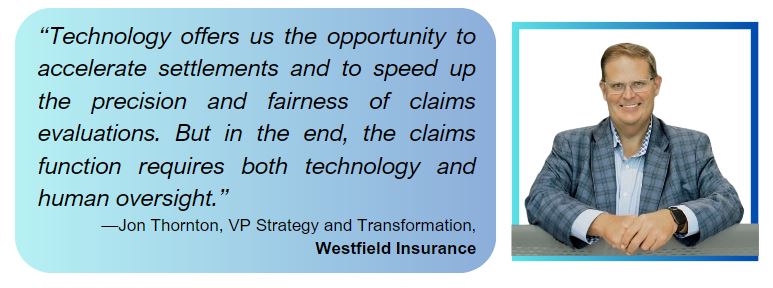

In a recent conversation with Auriemma Roundtables, Jon Thornton, VP Strategy and Transformation at Westfield Insurance, said that insurance shouldn’t aim to provide the kind of experience of the Amazons of the world.

“Our mission is to support customers after a loss,” Thornton said. “As claims professionals, we are trained to do the right thing. We put ‘boots on the ground’ to help our insureds recover from a disaster. Technology offers us the opportunity to accelerate settlements and to speed up the precision and fairness of claims evaluations. But in the end, the claims function requires both technology and human oversight.”

Thornton suggests an educated consumer is the answer and recommends two possible ways to address the current homeowners insurance crisis:

- Transparently share information with insureds about how prices are set and suggest ways to mitigate the risks.

- Use technology to break down data-sharing silos between underwriting and claims to encourage sharing of data. And ultimately, this information can and should be shared with insureds.

Case Study: The “Miracle House” on Maui

A striking NPR image from the recent Maui fire tells an important story: A 100-year-old house survived the Maui fire intact, while hundreds of others were destroyed. How did this house survive untouched?

It turns out that the owners of the house replaced the 100-year-old asphalt roof with a commercial-grade corrugated metal roof. The owners also cut back the brush and landscaping around the house and replaced it with river rock. The illustration makes the case dramatically about how “educated” homeowners can contribute to reducing their risks, given the right tools and information.

The technology – data and analytics, geo-spatial imagery, and AI – is available to help property insurers analyze property risks. On a property-by-property basis. Yet, individual homeowners are not aware of how underwriters assess the risks to their homes and, more importantly, homeowners do not know how to mitigate the risks facing them. A new approach to homeowners insurance could dramatically change the property insurance paradigm, moving it from ‘repair and replace’ to ‘predict and prevent’—if homeowners know the risks they face for wildfires, wind, and flooding, and were educated and rewarded by if they would take the necessary steps to mitigate and minimize the risks.

Claims professionals have a role in this challenge. One of the most effective ways to initiate change is to build a community of peers where claims professionals can share what works and what doesn’t work. One where sharing experiences both internally and externally will enable innovation to bubble up.

About the Auriemma P&C Claim Operations & Innovation Roundtable

Auriemma Roundtables combines claims executive meetings, industry-leading operational benchmarking, and peer group surveys to help participants identify tools, technologies, and strategies to offer best-in-class customer experiences at all touch points in the digital journey.

To learn more about how Auriemma’s Claims Operations & Innovation Roundtables can offer claims professionals the opportunity to innovate and improve the claims experience for insureds, contact Phylip Jones, Head of Business Development, Auriemma Roundtables.