12 E 49th St., 11th Floor, New York, NY 10017

T: +1-212.323.7000

E: info@roundtables.us

July 6, 2026

Beyond Complaint Volume: Why Credit Bureau Dispute Data Needs Context

The CFPB’s recent change to its consumer complaint system highlights a challenge that financial institutions know well: public complaint data does not always explain what is really happening operationally—or why.

Consumer complaint data has become one of the most closely watched indicators in financial services. But as complaint volumes climb, interpreting what the data actually means is increasingly difficult. Credit reporting complaints have become one of the clearest examples of how quickly public consumer data can become difficult to interpret. The Consumer Financial Protection Bureau (CFPB) recently underscored that challenge, noting that credit or consumer reporting complaints increased from approximately 150,000 in 2019 to more than 5 million in 2025.

The reasons for this more than 3,200% increase? The CFPB says credit repair groups, social media influencers, AI tools, and emerging credit-score businesses may be driving misuse of the complaint process. In response, the CFPB is revising complaint portal procedures, implementing identity requirements, clarifying closure definitions, aligning the complaint process more closely with FCRA obligations, and taking steps to address potential misuse of the complaint system.

The Bureau also acknowledged a key limitation of the portal itself: “The CFPB cannot rely upon the consumer complaint portal data as a reliable reflection of actual market conditions or actual consumer experiences.”

Auriemma Roundtables agrees that complaint volume is an important signal, but it cannot explain on its own whether institutions are seeing a true market shift, an operational pressure point, or simply natural fluctuations. Leveraging peer industry benchmark data in complaints, disputes, and operations, empowers FIs to move from tracking complaint volume to understanding root cause without the noise.

Public Data Shows Trends, But Not the Full Picture

Public complaint data can be useful for identifying broad areas of consumer concerns. But, as stated by the CFPB, its utility has clear limits: Public datasets do not distinguish repeat, frivolous, indirect, direct, or high-risk dispute activity in a way that allows for meaningful peer comparison. Mere complaint volume also does not show any context, such as how any one institution’s internal metrics compare with the industry.

Two institutions may experience similar complaint volume but face very different operational realities. One may be seeing a short-term increase driven by a specific campaign or third-party source. Another may be dealing with a broader rise in legitimate dispute activity, longer resolution times, or higher pressure on dispute teams.

Without benchmark data, those differences are impossible to see.

Two Benchmark Signals Worth Watching

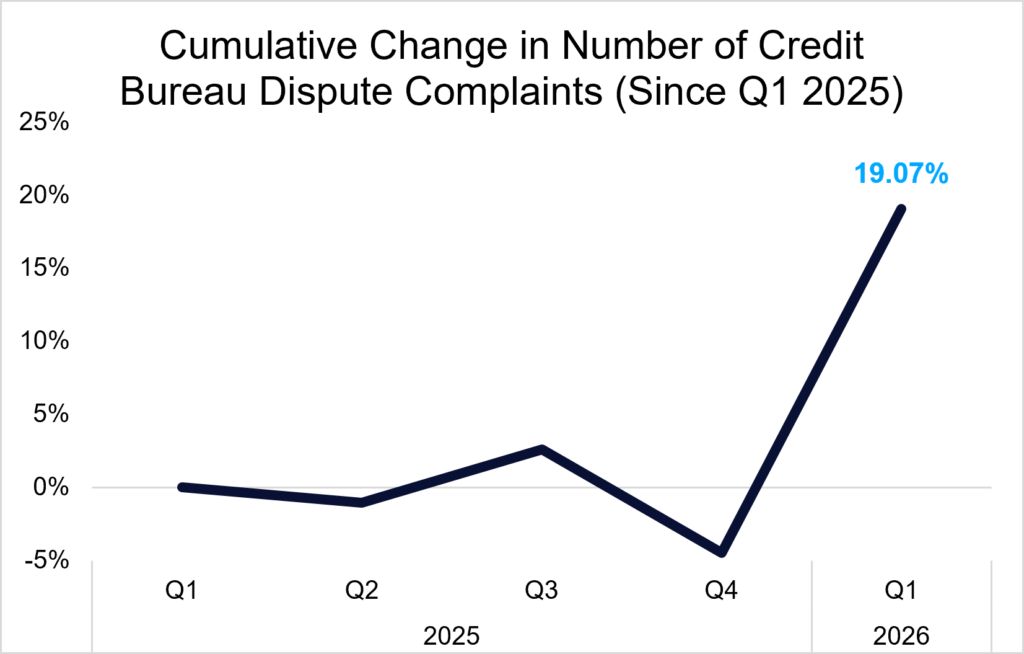

Benchmark data from Auriemma Roundtables’ Credit Bureau Roundtable shows one example of the kind of insight that public complaint data cannot fully provide. On average, banks reported 19% more complaints related to credit bureau disputes in Q1 2026 than in Q1 2025.

On its own, that increase is worth attention. But the real value comes from knowing whether this is a one-quarter blip, or the beginning of a larger trend.

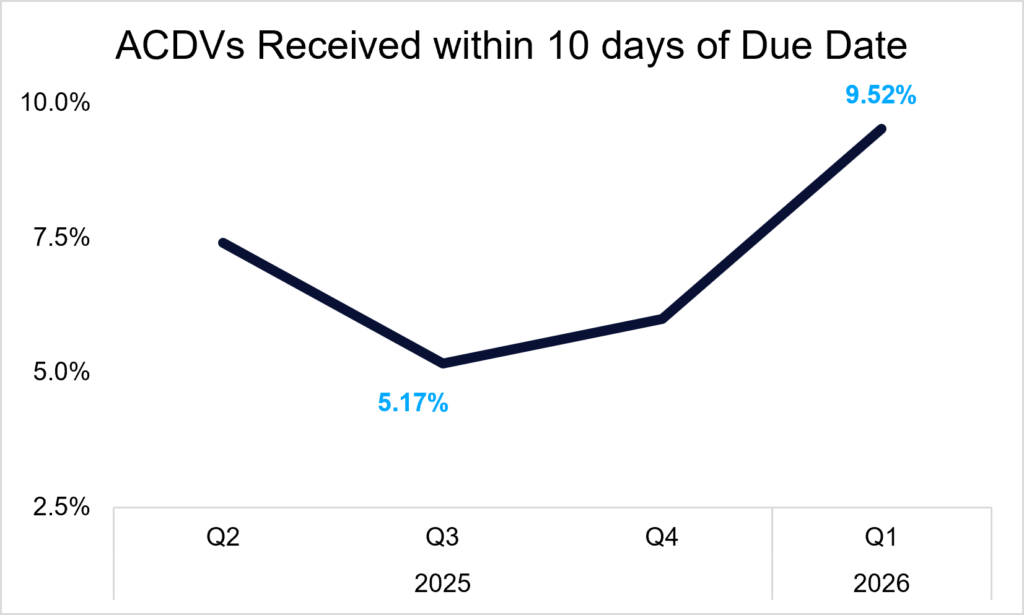

For example, over the same period, the share of Automated Credit Dispute Verifications received within 10 days of their due date increased from 5.99% to 9.52%. That does not necessarily signal a compliance issue, but it does point to a more compressed operating environment.

ACDVs received late in the response window leave less time for investigation, documentation, quality review, and submission. If a typical investigation takes closer to two weeks, more ACDVs arriving inside a 10-day window can create staffing strain and increase the risk of rushed handling.

While public complaint database can surface the signal, only peer-to-peer benchmark data helps institutions understand what that signal means and how to address it.

Why Peer Context Matters

The CFPB’s changes recognize that complaint data needs better structure, stronger identity protections, clearer closure definitions, and more consistent categorization. Those are positive steps.

But even with cleaner public data, financial institutions still need a more detailed view of how dispute and complaint activity compares across peers. Auriemma Roundtables’ benchmark data adds that layer by showing operational measures such as:

- Total disputes as a percentage of total tradelines at the bureaus

- Direct and indirect dispute resolution times

- Disputes per FTE

- Top reason codes for disputes

- Distribution of ACDV responses by response code

- ACDVs received within 10 days, 11 to 20 days, or 21+ days of due date

- Error, reject, and fatal error rates by credit reporting agency

Together, these measures help institutions understand efficiency, workload, data quality, response patterns, and operational risk.

Multiple Sources Create a Clearer View

Financial institutions need more than public complaint data to understand complaint and dispute trends. Internal reporting, peer benchmark data, and closed-door industry discussion help put activity in context and show whether changes are isolated, temporary, or part of a broader shift.

Auriemma Roundtables offers multiple ways to access that perspective, including the Credit Bureau Roundtable and the Multi-Vertical Complaint Management Roundtable. Together, these resources help institutions compare complaint volume, dispute activity, response patterns, staffing pressure, resolution performance, and peer approaches to complaint operations.

Contact Barry Lynch for more information on these Roundtables.

For more information on how benchmarking data can inform your complaint management strategy, reach out to Jared Kirby.